UV LED price decreases forcing a strategy review

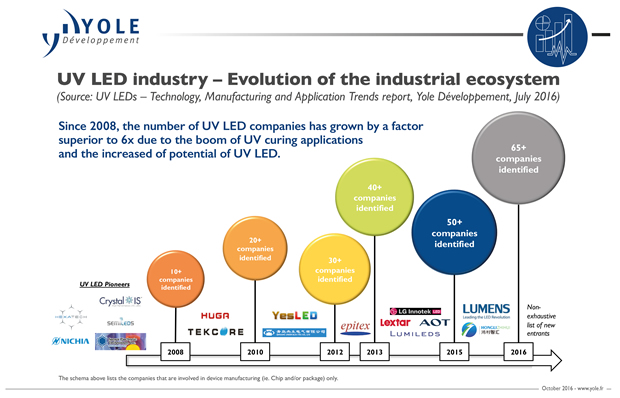

Yole Développement (Yole) has identified more than 65 companies involved in the UV LED industry for disinfection/purification applications in 2016. In 2012, the UV LED industry represented an industrial ecosystem of 30-35 companies thanks to the UV LED adoption for curing applications.

Since 2008, the number of UV LED companies has increased by more than six fold due to the boom of UV curing applications and the increased of potential of UV LED. This growth has been emphasised by the strong price-pressure environment in the visible LED industry, which began in 2012. The growth will be even higher in the next years, fueled by the price decrease…

The 'More than Moore' market research and strategy consulting company, Yole, proposes a technology and market report focused on the UV LED industry. Entitled UV LEDs – Technology, Manufacturing and Application Trends, this report reviews the global UV LED industry, from substrate to system and provides insights into the modification of the supply chain including new entrants, mergers and acquisitions.

UVA still represents the largest UV LED market today. However the future could be different due to the increase of UV LED performances: UV LEDs enable applications inaccessible to UV lamp. And if these applications take off, they could represent an additional revenue of nearly $143m in 2021. “The introduction of the semiconductor industry technologies and related value chains within the traditional UV lighting industry has redistributed value across the supply chain. It creates a large window of opportunity for entrants in the UV lighting applications using LED as a disruptive technology,” said Pars Mukish, Business Unit Manager at Yole.

“The recent UV LED price decreases are forcing manufacturers to review their strategy”, commented Pierric Boulay, Market and Technology Analyst at Yole. “The visible LED industry is suffering from strong price pressure. As a result LED manufacturers are looking at opportunities to increase their revenues and margins.” In this context, the UV LED market has been perceived as a potential ‘blue ocean’ of attractive opportunity for these players.

Since the 2012 boom of UV curing applications, more than 55 LED companies have entered the UVA LED industry. Today the UVA LED industry is well structured, with a large number of suppliers, and the price and performance of devices in greater agreement with application level requirements. A good symbol of this maturation is the involvement of six of 2015’s top-10 visible LED players: Nichia, Lumileds, Seoul Semiconductor/Seoul Viosys, Everlight, LG Innotek and Lumens.

So what’s next? Will the UVA LED industry follow the same trend as the visible LED industry, a blue ocean that turns into a bloodbath? In four years, the number of manufacturers has increased five or six fold, with most of the new entrants coming from Taiwan and China. The emergence of these players has already had an impact on the industry, forcing all manufacturers to dramatically reduce their prices and margins in 2015.

The industry can only handle such price reductions and intensifying competition if the market can offset it, for example through a volume increase. But it is likely that several players will exit the business, unable to develop as required. Indeed, UV LED device development seems to have reached a limit because manufacturers use techniques developed in the visible LED industry. Further performance improvements and price reductions will therefore require strong R&D investment. This trend will benefit big players that are more able to make the necessary financial commitment. Smaller players, if they want to survive, will have to differentiate themselves or develop different strategies. Vertical integration up to the module/system level could represent the best opportunity for them to generate additional revenues.

The UVA LED supply chain is now well structured. This market segment is showing six of the top ten visible LED players in 2015 that have a strong foothold in this business. All companies are developing specific strategies to maintain their positioning and business. In relation to the UVB/UVC supply chain, it is now becoming more mature step-by-step and is more structured. Indeed, current technologies point out good performance and players enlarge their manufacturing capacities. According to Yole’s analysts, recent joint ventures and mergers and acquisitions occurred mostly in the UVB/UVC LED industries. Indeed objectives were to get an access and/or secure technologies.

Yole’s UV LED report presents a detailed analysis of the industry, including: main players by wavelength range from UVA to UVB and UVC. As well as their positioning in the value chain, and recent trends. This analysis is also a comprehensive overview of UV LED device manufacturing, describing UV LED structures, current challenges and key research directions. In addition, the report analyses the UV LED performance and price roadmap.

Product Spotlight

APV1111GVY

Panasonic

Panasonic PhotoMOS® Photovoltaic MOSFET High-Power Drivers

| SKU: | |

|---|---|

| Stock: | 3490 |

| Cost: | $3.95 |